Source: U.S. Energy Information Administration, Annual Energy Outlook 2013.

Note: MSW is municipal solid waste.

Note: MSW is municipal solid waste.

On April 15, the Internal Revenue Service (IRS) released guidance clarifying the eligibility for the recently extended renewable electricity production tax credit (PTC). Congress passed the extension on January 1, 2013 as part of the American Taxpayer Relief Act of 2012 (ATRA). EIA expects this extension could result in significant wind capacity additions over the next three years, leading to higher generation from wind.

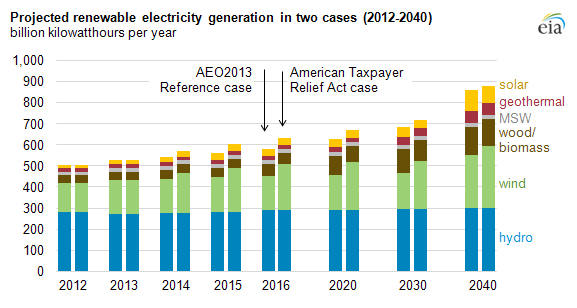

Compared with the Annual Energy Outlook 2013 Reference case, which does not include reference to ATRA, the extension of the PTC increases renewable generation through the projection period, but the effect varies greatly over time. In the near term, ATRA leads to a large increase in wind generation, up by 34% in 2016 compared to the reference case. Total projected renewable generation is 9% higher in 2016.

ATRA extended several tax credits to the energy sector (among other things), including the tax credits for utility-scale renewables, residential energy efficiency improvements, and biofuels. EIA's analysis of ATRA found that the most significant impact on energy markets came from the extension of the PTC for wind projects.

A crucial new feature of ATRA is the relaxation of the requirement in previous versions of the PTC that a qualifying wind project be in service by a specified date (most recently, the end of 2012). Instead, ATRA requires that qualifying wind projects be under construction by the end of 2013.

The April 15 IRS guidance defines a plant as "under construction" if it has either started "physical work of a significant nature" or if it has incurred at least 5% of the project's estimated total cost. EIA's analysis assumes that the effective length of the PTC extension is equal to the typical project development time for a qualifying project, or roughly three years for a wind project.

Although EIA projects that ATRA will result in significant near term capacity and generation growth, by 2040 the difference in projected renewable generation between the Reference and ATRA cases is only 2% (wind is up by 17%). These results indicate that, while the short-term extension does result in a net increase in wind generating capacity, some construction that otherwise would have occurred later in the projection period is simply completed earlier to take advantage of the extended tax credit. The increase in wind generation partially displaces other forms of generation in the Reference case, both renewable and nonrenewable, particularly solar, biomass, coal, and natural gas.

Although EIA projects significant short-term growth in wind capacity under ATRA—about 20 gigawatts between 2012 and 2016—the exact timing of the short-term capacity additions is still relatively uncertain. Following thebuildup in capacity completions leading up to the expected PTC expiration at the end of 2012, the first quarter of 2013 saw very little wind project development activity. As developers have a chance to react to the new IRS clarification, EIA expects that power purchase agreements and financing activity will resume, and the timing of this resumption likely will affect the timing of building new capacity in the near term.

Further detail on EIA's analysis of ATRA and other policy-related side cases can be found in the full Annual Energy Outlook 2013.

Source: EIA

Source: EIA

No comments:

Post a Comment